You Don't Need $1M to Retire — You Need $1M Working For You

I ran the math on the 4% rule, the 8% rule, and income investing. The results changed everything.

How much money do you need to retire?

If you’ve ever Googled that question, you’ve probably landed on the same answer everyone else gets: save a million dollars. Maybe two million. Follow the 4% rule. Don’t touch the principal. Hope it lasts.

But here’s what nobody talks about. Two people can retire with very different amounts of money — and the person with LESS can actually end up with MORE income, more security, and more money left over at the end.

I ran the math. And the numbers completely changed how I think about retirement.

Before I get into it — I want to hear from you. When do you want to retire? And more importantly, what’s your plan to create income when you do? Leave a comment. I’m asking because I’m already there. I retired from corporate in 2023 and I’m living off my portfolio income right now — while continuing to build my snowball so I can keep traveling and living life on my terms.

I’m not asking from the sidelines. I’m in it.

Quick disclaimer — I’m not a financial advisor. Everything I share here is what I’m personally doing and researching in my own portfolio. This is education, not advice. Always do your own research before putting your hard-earned money to work.

Where the 4% rule came from

If you’re going to follow a rule, you should at least know who wrote it and why.

In 1994, a financial planner named William Bengen published a paper called “Determining Withdrawal Rates Using Historical Data.” He looked at every 30-year retirement period going back to 1926. The Great Depression. World wars. Stagflation in the ‘70s. Every major market crisis.

His question was simple: what’s the most a retiree could withdraw each year — adjusted for inflation — and never run out of money over 30 years?

His answer: about 4%.

Four years later, three professors at Trinity University in Texas ran a similar study. Same conclusion. And the “4% rule” was officially born.

Here’s the thing. That research assumed a 60/40 portfolio — sixty percent stocks, forty percent bonds. It assumed a 30-year retirement window. And it was built using data where bond yields were significantly higher than what we see today.

This rule was designed over 30 years ago, using market conditions that no longer exist, for a retirement window that many people will outlive.

And yet — it’s still the default advice for millions of Americans.

What the 4% rule actually requires

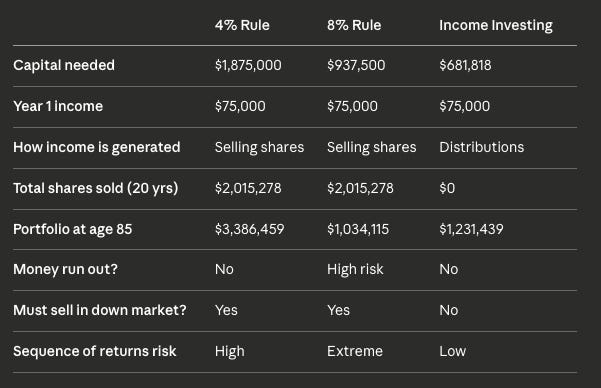

Let’s run the math with a real number. Say your lifestyle costs $75,000 a year. That’s what you need to live comfortably.

Under the 4% rule, you take your annual need and divide by 0.04.

$75,000 ÷ 4% = $1,875,000.

You need nearly two million dollars saved before you can retire.

And here’s the part that really gets me. Every single year, you have to SELL your investments to generate that income. Year one — you sell $75,000 worth of stock. Year five — you’re selling $84,000 because of inflation. Year ten — nearly $98,000. Year twenty — over $131,000.

Over 20 years — from age 65 to 85 — you will have sold over $2 million worth of assets just to live.

In a perfect world with a steady 7% average return, the math works. Your portfolio actually grows to about $3.4 million by 85. But here’s the catch — you had to start with $1.875 million, you had to sell assets every single year, and you’re sitting on a fortune at the end that you’ll probably never spend.

That doesn’t sound like freedom to me. That sounds like a savings account with extra anxiety.

The 8% rule — same problem, bigger risk

Now let’s talk about the 8% version. This has been making the rounds in FIRE circles and from some well-known financial personalities. The argument: the stock market averages 10 to 12% per year, so why not pull 8%? You’re still leaving a cushion.

$75,000 ÷ 8% = $937,500.

Half the savings needed. Same lifestyle. Sounds great.

In a perfect world — smooth 10% returns every year — it works. Your portfolio stays above a million the entire time.

But the world is not perfect. And this is where the 8% rule falls apart.

I ran a scenario where a bear market hits in the first three years of retirement. Down 20% year one. Down 15% year two. Up only 5% year three. After that, the market returns to a normal 10%.

Your money runs out at age 75.

Ten years into retirement. Gone. Zero. You’re 75 years old with no portfolio, no income, and a decade of life left to fund.

That’s not a worst-case fantasy. Bear markets at the start of retirement have happened multiple times in the modern era. It’s called sequence of returns risk. And if you’re withdrawing 8% when it hits, it will destroy your plan.

The 8% rule works on a whiteboard. It does not work in the real world.

The third approach — income investing

What if instead of saving two million dollars and slowly eating it... you built a portfolio that PAYS you?

Not by selling shares. Not by drawing down your nest egg. But by collecting distributions — real cash — from investments designed to generate income.

This is income investing. And it changes the entire equation.

Same $75,000 lifestyle. But instead of withdrawing 4% or 8%, I’m collecting income from a blended portfolio yielding around 11%.

$75,000 ÷ 11% = $681,818.

Less than $700,000. Not two million. Not even a million. Under seven hundred thousand dollars — to generate the same $75,000 per year.

And here’s the difference that changes everything. You never sell a single share. Your income comes from distributions. Dividends hitting your account every week or every month.

Over 20 years, you collect the same $2 million in total income. But you sell zero dollars in assets. Zero. And with even a conservative 3% price appreciation, your portfolio grows from $682,000 to over $1.2 million.

The 4% rule needs $1.875 million and still requires selling assets every year. Income investing needs $682,000 and you keep every share you own.

Same lifestyle. Less than half the starting capital. No selling. And you end with MORE money.

That’s not theory. That’s math.

The side-by-side comparison

Here’s all three approaches laid out for a $75,000/year lifestyle from age 65 to 85:

Assumptions: 4% rule uses 7% avg return (60/40 blend). 8% rule uses 10% avg return (100% equities). Income investing uses 11% distribution yield with 3% price appreciation. All scenarios adjust for 3% annual inflation. Past performance is not a guarantee of future results.

Same income. Same lifestyle. Completely different outcomes depending on the approach.

Why this works — and how I structure it

I’m not going to pretend this is magic. There’s no free lunch. Income investing has its own risks — NAV erosion, distribution cuts, sector concentration. I’ve been burned. I’ve talked about those lessons before.

But here’s what I’ve learned: the risk isn’t in the income. The risk is in not having a structure.

That’s why I use what I call the 3-Bucket System: an Income Engine for high-yield funds that pay the bills today, Core holdings for stable broad market income, and a Defensive Moat for protection when markets get ugly. I’ll be doing deeper dives on each of these in future posts.

And I use the PLAN framework: Purpose and Patience. Learn the Landscape. Asset Allocation. Net Income Focus. Every dollar has a job — and the PLAN makes sure those jobs are assigned with intention, not impulse.

Here’s what this looks like in real life. My portfolio is sitting at $875,000. It’s generating $222,749 a year in passive income. That’s over $18,500 a month. And my yield is sitting at 25.45%.

Now — I know what some of you are thinking. 25%? That sounds aggressive.

You’re right. It is. On purpose.

I’m in what I call the building phase. I retired from corporate in 2023, but I still have part-time active income — coaching, content, projects I choose to take on. That active income covers my lifestyle right now. Which means every single dollar my portfolio generates gets reinvested. Every distribution goes right back in — growing my snowball, adding to my core positions, compounding.

Because I still have active income as a safety net, I can afford to carry higher-yield, higher-risk positions in my Income Engine bucket. I’m using that yield to accelerate the build. That’s the whole point of the building phase — you take strategic risk while you can absorb it.

But here’s the important part. When I’m ready to fully step away — no more active income, no more side projects — I’ll rotate out of those aggressive positions and into my Core and Defensive buckets. SPYI. QQQI. MLPI. IAUI. Funds that yield 10 to 14% with more stability and less volatility.

That’s the transition. Building phase to income phase. Acceleration to sustainability.

And that’s exactly why I used 11% in the scenario math — because that’s the yield range of a fully rotated, retirement-ready income portfolio. Not 25%. Not the aggressive stuff. The Core. The Foundation. And even at 11%, the math crushes the 4% rule.

I don’t sell a share to fund my life. My distributions pay for everything. And right now, while I’m still building, those distributions are making the snowball bigger every single week.

The real question

The 4% rule asks: how much can I afford to spend before my money runs out?

Income investing asks: how do I build something that pays me forever?

One is a countdown. The other is a system.

I know which one I chose.

I want to hear from you — which approach makes more sense? Are you still following the 4% rule? Have you started building your own income snowball? Drop a comment below.

📺 I made a full video breaking this down with visuals, charts, and the complete math walkthrough. Watch it on YouTube here.

🧮 Want to figure out your own freedom number? My Freedom Calculator is completely free — it helps you determine how much income you need and your timeline to get there. Grab it here.

If it doesn’t challenge you, it doesn’t change you. Messy action is better than no action.

— Rico

Wife and I are planning on 6%. Half of our portfolio in S&P 500 Index ETFs and 50% in Income generation ETFs (SPYI and QQQI). Since we're in our 50's, we'll need to use 72(t) distributions to access our retirement plans.

Your title says it all!