I Lost Everything in 2009. Here's What I'd Tell That Version of Me.

Bankruptcy didn't break me. It built me.

In 2009, I filed for bankruptcy.

I owed more than I could count. I lost my home. I was paying over $900 a month — for five years — just to dig out of a hole I dug with my own hands.

Today, I’m collecting over $16,000 a month in passive income. I retired on my own terms in 2023 after 20+ years as a creative tech executive at companies like Netflix, Zappos, and Outschool. I’m building an income portfolio that pays me whether I wake up at 6 AM or noon.

So how do you go from bankruptcy court to that?

That’s what this article is about. Not the ETFs. Not the tickers. The real story underneath all of it — and the lessons that made everything else possible.

Quick Disclaimer

I’m not a financial advisor. I’m just a guy sharing his real story and what I’ve personally learned along the way. This is education, not advice. Always do your own research before putting your hard-earned money into anything.

2006 Rico

Let me take you back.

It’s 2006. I’m working at Zappos. Good job. Steady paycheck. And I’m feeling confident. Maybe too confident.

I wanted to buy a house. The problem? I didn’t really have the money for a down payment. But back then, the lending environment made it easy to pretend you did. Predatory lending was everywhere — and I walked right into it.

I did what’s called an 80/20 loan structure. One loan for the primary mortgage. A second loan to cover the down payment. Two loans. Zero equity. One hundred percent leverage.

And I didn’t stop there.

At the same time, I started a brick-and-mortar business with a partner. Retail. Right before the Great Recession — though obviously I didn’t know that yet. Nobody puts “economic collapse” on their business plan.

To fund that business, I took out a HELOC — a home equity line of credit — on a house I already couldn’t really afford.

Let me add that up:

Primary mortgage — loan number one.

Down payment loan — loan number two.

HELOC to fund a business — loan number three.

Credit card debt from the business — over $70,000.

I was over-leveraged. I was more optimistic than realistic. And I was using debt as a backstop instead of a tool.

That’s a big distinction. And it took me years and a lot of pain to understand it.

The Fall

Then 2008 happened.

The recession hit. The business didn’t make it. We closed the doors. The housing market collapsed. And suddenly I was sitting on a pile of debt with no way to service it.

My business partner was able to file Chapter 7 — a full liquidation. She had no assets, so the court essentially wiped the slate clean for her. But here’s the thing — I had co-signed on those business loans. Her slate was clean. Mine wasn’t.

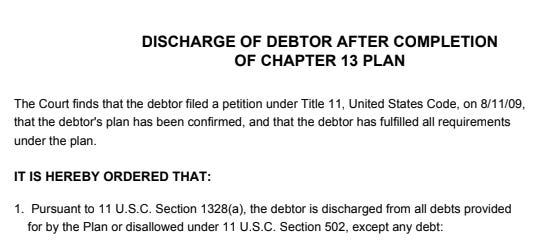

I was still working full-time. I still had income. So Chapter 7 wasn’t an option for me. I had to file Chapter 13 — which is a structured repayment plan.

What does that mean in real life?

It means a court tells you how much you owe, how much you’re paying, and for how long. Every month. No exceptions. My payment was over $900 a month. For five years. And here’s the part people don’t realize about Chapter 13 — the more you make, the more your payments go up. There’s no reward for earning more. The court adjusts.

By the time it was all over — January 2015 — I’d paid back roughly $80,000. Five and a half years of my life under court supervision. Every dollar accounted for. Every raise monitored.

I’ll be honest — that period humbled me in ways I’m still processing. But it also taught me things no book, no YouTube video, no course could’ve taught me.

What I’d Tell That Version of Me

If I could sit across from 2009 Rico and talk to him, here’s what I’d say.

On Debt

2009 Rico thought debt was how you got ahead. Borrow to buy. Borrow to build. Borrow to bridge the gap.

2026 Rico knows debt is a tool — and like any tool, it can build you up or tear you apart depending on how you use it.

The difference? I understand leverage now. Real leverage. Not the kind where you stack loans on top of loans and hope the market cooperates. The kind where every dollar you deploy has a job — and that job is to generate income.

Every dollar has a job. That phrase means something completely different to me now than it would have in 2006.

On Risk

2009 Rico confused optimism with a plan. I was excited about the business. Excited about the house. Excited about the future. But excitement isn’t a strategy.

2026 Rico manages risk with structure. I have a 3-Bucket System. I have stop losses. I have exit strategies. I know what I’m willing to lose before I enter a position — not after.

From my experience, the moment you say “it’ll probably be fine” is the moment you need a plan the most.

On Co-Signing

Here’s a lesson I paid $80,000 to learn.

When you co-sign debt, you’re not supporting someone else’s dream. You’re taking on 100% of the liability with 0% of the control.

My business partner walked away clean. I spent five years paying it back. That’s not a complaint — it’s a fact. And it’s a fact I want you to hear if you’re ever in a position where someone asks you to co-sign.

On Starting Over

Maybe the biggest one.

2009 Rico felt like a failure. Like the bankruptcy defined him.

2026 Rico knows it was the foundation. Not the failure — the foundation. Everything I’ve built since then — the discipline, the systems, the portfolio — started in that five-year window where I had no choice but to learn.

You don’t build an income snowball without understanding what it feels like to watch money disappear. That’s not something I read in a book. That’s something I lived.

The Rebuild

My Chapter 13 was discharged in January 2015. I have the court document to prove it.

But “done” didn’t mean “fixed.” My credit was wrecked. My confidence with money was shaky. And I had to completely rebuild my relationship with debt and leverage from scratch.

By 2017, I’d gotten my credit score back to a decent place. And this time, I came at it differently. I wasn’t guessing anymore. I understood the difference between debt that drowns you and leverage that builds you.

I started investing in real estate with a partner. We built that portfolio up to over 30 units. Real leverage this time — income-producing assets with cash flow, not speculative bets with borrowed money.

Then COVID rolled around. We started selling properties for profit. And I rolled those proceeds into what you see today — my income portfolio. The income snowball.

I still have 4 rental units. I have a rollover 401k. A Roth IRA. My income portfolio. Even a fun account where I hold Rivian because you’ve gotta have a little fun with it.

But the core of everything — the engine that lets me live on passive income — started with lessons I paid $80,000 to learn in a bankruptcy courtroom.

There’s a much deeper story here about the real estate journey and the specific decisions that took me from discharged debtor to retired at my own choosing. If you want to hear it, reply to this article or drop a comment — I’ll write that one next.

Why I’m Sharing This

I share my portfolio numbers every month on this channel. I show the wins. I show the losses. I show the ETFs, the yields, the distributions.

But none of that means anything without context. And this is the context.

The income snowball I’m building right now exists because of what I lost in 2009. The systems I use exist because I once had no system at all. The discipline exists because I once had none.

If you’re starting from zero — or from below zero — I want you to know that’s not the end of your story. It might be the most important chapter in it.

If you want to see this story come to life, I recorded a full video version on my YouTube channel. [Link to video]

And if you’re working on building your own income snowball, my Freedom Calculator is completely free. It can help you figure out your freedom number and your timeline to get there. You’ll find it right here on Substack.

— Rico